Innovaccer is a healthcare technology company pioneering the Data Activation Platform that’s helping the industry realize the promise of value-based care.

Innovaccer’s integration & analysis engine activates healthcare data, cleaning, aggregating and delivering insights at the moment of care. This revolutionary technology streams analytics with custom insights and dashboards, automates workflows, provides real-time decisions for care teams, and point-of-care alerts—actionable intelligence without leaving the EHR experience.

Innovaccer is based in San Francisco with offices across the United States and Asia.

What is the single-most innovative technology you are currently delivering to health systems or medical groups?

Innovaccer is a leading healthcare technology company that deploys its FHIR-enabled Data Activation Platform to help the healthcare industry realize the promise of value-based care. The name “Innovaccer,” is, in fact, a play on the words “innovation” and accelerator.”

Innovaccer leverages AI and predictive analytics to generate insights that help healthcare organizations achieve better clinical outcomes. The FHIR-enabled Data Activation Platform is built on a Hadoop-based Big Data repository with a scalable architecture that allows the integration of disparate sources of data without having to write code. Its agile and modular structure can ingest structured, semi-structured, unstructured data, pool it as a single source of truth, and work on a central HL7 FHIR-based data schema.

How is your product or service innovating the work being done in the organization to provide care or make systems run smoother?

Innovaccer’s smart FHIR-enabled Data Activation Platform has intelligent workflows powered by unified patient records, advanced analytics and true interoperability, enabling collaborative healthcare. Innovaccer brings the data and all healthcare stakeholders together and empowers them with complete patient information to help them care as one.

Today, Innovaccer’s COVID-19 Management System uses AI to optimize the provider response to the disease, allowing medical facilities to reduce assessment time and prioritize patients with a high-risk profile for the next steps of care.

By Mike Sutten, chief technology officer, and Dr. David Nace, chief medical officer, Innovaccer.

Burdensome documentation and gaps in care have been long-standing challenges in the healthcare industry.

The COVID-19 pandemic has amplified those challenges on a global level, creating a situation in which people have been hesitant to seek care for other medical concerns. As such, healthcare providers are losing revenue, employees are losing their jobs, and those remaining in the workforce are subject to burnout.

In an effort to prevent the spread of COVID-19, many healthcare providers proactively reduced or stopped in-person visits for non-COVID-19 medical needs, ranging from the routine care of a sore throat to treatment of chronic conditions, cancer, and even mental health services.

Additionally, nearly one-third of American adults reported delaying or avoiding medical visits over concerns for possible exposure to the virus, according to an American College of Emergency Physicians and Morning Consult poll. More than half reported worrying about access to their primary care physician or being turned away from the hospital.

As a result, healthcare spending decreased by 18% in the first quarter of 2020, according to the U.S. Bureau of Economic Analysis. Surprisingly, some 1.4 million healthcare workers lost their jobs in April, a sharp increase from the 42,000 reported in March, according to the U.S. Bureau of Labor Statistics.

The global pandemic amplifies the day-to-day challenges of identifying gaps in care, the increased documentation required to track them, and the difficulties associated with determining their effects and responding with appropriate interventions.

The impact of this virus looms over the backdrop of a healthcare environment in which the American Hospital Association (AHA) makes the point is rapidly evolving from a fee-for-service system into a value-based delivery system. As healthcare providers and payers transition to collaborative digital care delivery models, this movement highlights the greater need for a data infrastructure that supports value-based care with sharper and more transparent insights into population health.

The health plan market is undergoing a drastic transformation. In the past, the competition had been lean with just a small number of payers. However, the market dynamics are changing. Since 2017, the number of MA plan choices per county has increased by 49%. The competition is said to grow even more in the coming years as more health plans are set to enter the market, owing to the fact that nearly 26 million baby boomers will age into Medicare through 2030.

Rising cost burden on health plans

With additional members, the “paperwork” and administrative costs are also increasing. A recent report revealed that there was almost a 6% increase in administrative expenses for MCOs in 2017. The substantial rise in membership with soaring costs means many health plans might find themselves in a financially untenable situation.

Along with the growing administrative burden, the compliance requirements are also weighing on the workload and costs. The push towards improving accuracy, completeness, and timeliness of the data is intensifying to “ensure that provider claims for actual health care spending matches the health plans reported financially,” said Seema Verma. To fulfill the reporting requirements and avoid financial penalties, health plans will have to improve their data submission process to align with the specific rules, formats, and regulations of a given state, which also ensures an increase in cost.

Payers don’t have much control or influence on the administrative and compliance costs. The member population will increase, and so will the requisites by regulatory authorities. The costs are likely to keep increasing on these fronts in the future.

The growing financial pressure has made it inevitable for payers to explore measures to contain costs from spiraling out of control. Since operations account for around 50% of an insurer’s base cost, reducing expenses on this segment can result in cost savings of significant proportions.

Resolution for cost pressures: Operational efficiency

There are certain operational activities such as claims adjudication, reprocessing, and post-call documentation which are highly repeatable and are executed manually. With the addition of more members each year, the burden of these tasks ought to grow even more. Automating these tasks can give a significant boost to operational efficiency; at the same time, it can help reduce overall costs. According to an article, automation technology can lead to an additional operational cost savings of up to 30 percent within five years for many payers.

Outcomes of automating operational activities

Apart from cost savings and reduced utilization, automating operational tasks has multiple other advantages. Automating routine tasks can ensure that the tasks that previously took days to finish are completed in minutes. The accelerated service delivery can build more synergy between members, providers, and internal stakeholders.

Rising healthcare promises have been tied to cloud technology in the most recent tech-talks of the town. While the majority of care providers are not holding their breath due to previous disappointments, we wanted to translate the often vague statements made into discrete simplified processes for healthcare.

Healthcare is riding a wave of digital transformation that has brought about revolutionary processes of data management and care delivery. Moving from paper-based records to a digital format, the first wave took us from disconnected facility-based care to integrated smart care with increased coordination and population health activity.

The second wave enabled better patient experience with omnichannel communications and interoperable data sharing applications. Empowering patients and clinicians with analytics, the recent wave has health organizations leveraging real-time data-driven solutions, artificial intelligence, and cloud services to align with the culture of preventive and wellness-centric care.

The cloud will be central to future digital transformations in healthcare. What is uncertain for many is what specific, new cloud services will be developed and why are healthcare organizations now – and foreseeable future continuing – to opt for cloud-based technologies.

Why are health organizations leveraging the cloud?

We have been in the process of transitioning from fee-for-service to value-based care over the past decade. The industry is further planning to move from disease-based episodic care to preventive care in future years. To achieve that goal, several additional factors need to progress.

The healthcare system of the future will be more consumer-centric and value-driven. It will use real-time data to generate actionable insights, and data technology will play a crucial role. Cloud technology promises to improve performance enhancement and healthcare data analytics overall.

Health systems have a need for increased data capacity, and the cloud promises almost unlimited data storage, easy accessibility, and enhanced cybersecurity. As health organizations are expanding into a variety of digitized services such as virtual care, wearable devices, telemedicine, and smart AI assistance, the data per patient expands.

The cloud is a single point of access to patient information, to multiple doctors and medical services at the same time, that boosts not only real-time coordination but also ensures data security for hospitals and patients.

Gartner, in a recent healthcare cloud services report, highlighted how provider leadership has moved from skepticism to acceptance of the cloud as a service delivery model. In what ways is the cloud benefiting the healthcare industry?

After the enactment of the Affordable Care Act, insurers had to cut down on the “cherry-picking” of members and not provide insurance to just low-risk individuals. To some extent, the scope for earning high-profit margins had decreased for health insurance companies. This rule created an imperative for them to look for ways to curb expenses in other ways.

As a result, influential insurers came up with an innovative idea to merge with their contemporaries. Mergers and acquisitions reduce the competition and empower payers to negotiate better with the providers.

However, a lot of Medicare Advantage (MA) markets are served by just one or a small number of insurers and the competition is already bleak. If the few existing insurers also lobby to negotiate contracts, the providers wouldn’t stand a chance to get a decent deal.

US healthcare dynamics are already far from ideal with costs soaring high and quality parameters below most developing nations. The lopsided power play between providers and payers can exacerbate the existing healthcare problems.

To prevent this, the government is making it a point to put brakes on major insurance mergers and acquisitions. At the beginning of 2017 U.S. District John D. Bates ruled against Aetna’s acquisition of Humana. Along with that, the Anthem–Cigna merger was also stopped from going through. It seems like it’s time for payers to think beyond this strategy of creating an oligopoly. It also means that insurers have to compete with each other instead of relying on their collective clout.

Gaining an edge over competitors with improved star ratings

Now that there is no way for insurers to earn strong profits other than by capturing increased market share, they need to look for ways to increase the number of enrollments. For MA plans, their best shot to grow their member enrollments is by achieving credible star ratings. Medicare’s Star Rating system was developed to provide Medicare beneficiaries some concrete insights about a plan’s performance. Every year, CMS evaluates the performance of each MA Plan on quality and cost measures and rates them on a scale of one to five stars. The more stars a plan gets, the more appealing it appears to the beneficiaries, which leads to increased enrollments.

Every health plan aims to achieve maximum operational and cost efficiency and tries to create lucrative offerings for the members. However, unless they are able to do it better than other health plans, their efforts will not bear fruit. The first step to improving their Star ratings is to assess the performance measures of other health plans.

Evaluating the performance of MA plans over the last few years

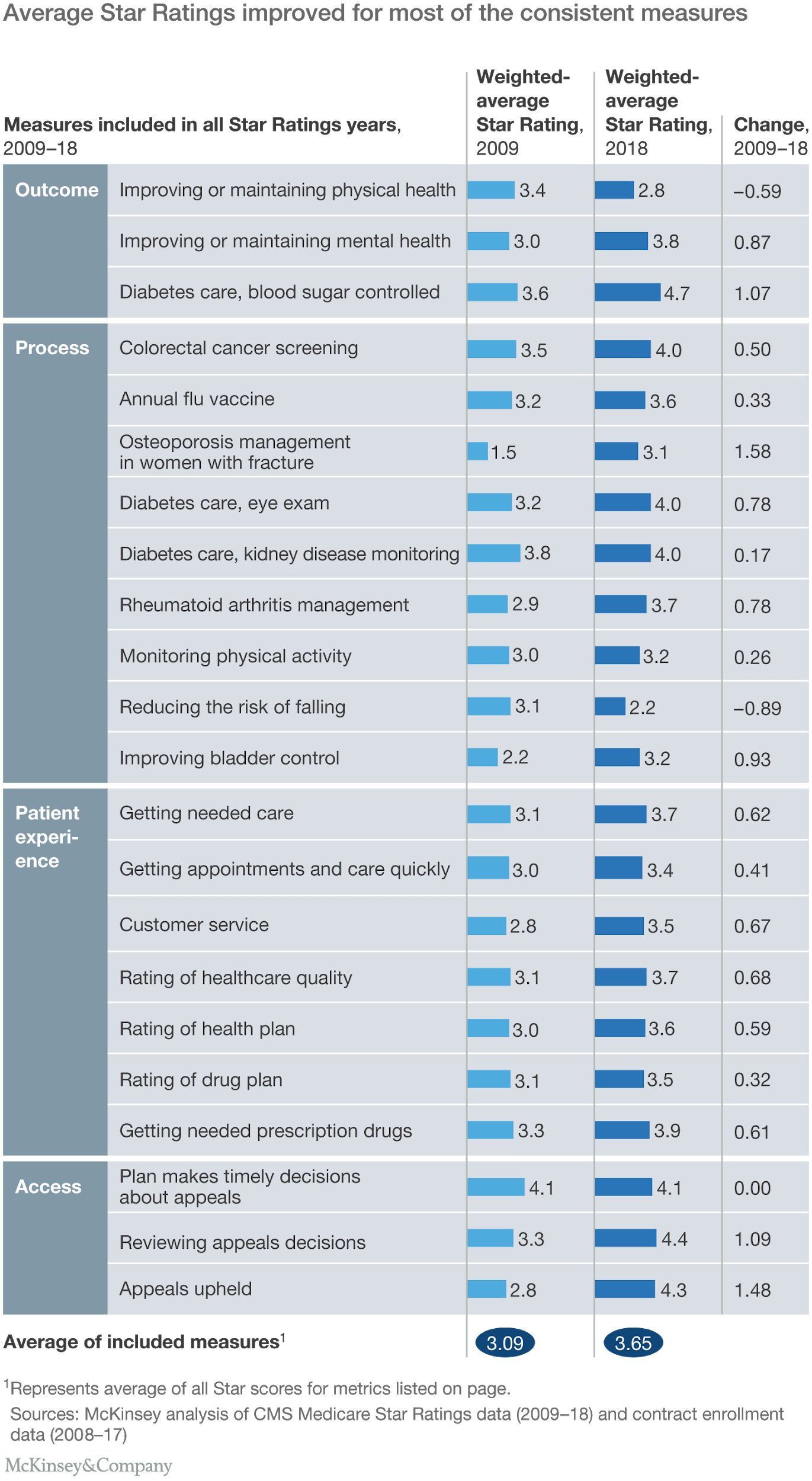

In 2011, only 24 percent out of all MA Plans got 4+ Star Ratings. By 2018, this figure grew almost by a whopping 50 percent. In a bid to perform better, the health plans brought remarkable changes in their performance. As a result, member enrollments also increased by 17 percent in this tenure.

Since the inception of the Medicare Advantage, some measures were modified. However, there were 22 measures that remained consistent between 2009 and 2018. On calculating the average Star ratings of each measure, it was revealed that the average Star ratings had improved by 0.56. The average outcome measures had improved by 0.45 stars, the process measures by 0.49 stars, the patient experience measures by 0.55 Stars and the access measures by 1.12 stars.

Overall, most of the measures showed some improvement. Since 73 percent of the health plans have ratings above 4 Stars, it can be established anything below this can gravely impact the number of member enrollments. On top of that, to match the average performance scores of other health plans, health plans have to earn an average of at least 3.5 Stars.

Creating strategies to perform better than other health plans

An overarching picture of how all the MA plans in the country are performing can be helpful in revealing the measures you need to work on. However, understanding the area-specific operational nitty-gritty is important to find out what steps you need to take to improve the performance of your health plan.

Comparing your plan with top-performing health plans in your area and diving deeper into their measures can unveil what they are doing to perform better than others. This information can be instrumental in devising winning strategies to score star ratings that are better or at the very least at par with other high-performance plans.

The provider community strives day and night to improve patient outcomes and contribute to the dream of value-based healthcare. However, the complexity of chronic diseases renders strategies ineffective and prevents them from reducing available utilization. In the US, chronic diseases account for 75 percent of all healthcare spending, to the tune of $3.5 trillion. In fact, every 6 out of 10 US adults is living with a chronic condition.

And, the costs are going to inflate in the future as well

By 2030, there will be more than 77 million+ people above 65 that necessitates Medicare coverage, which also calls for better chronic care management measures. If high-risk populations are identified now, the US healthcare can be better prepared to meet care expectations in the future and contain the costs for good. That said, a myopic approach to chronic care isn’t going to cut it. Let’s take a look at the loopholes in current chronic care management programs.

Pitfalls in Chronic Care Management

Fixation on short term goals

Effective chronic care management requires providers to focus on long-term well-being and stabilization needs of patients. However, the Affordable Care Act incentivizes providers for a reduction in 30-day re-admissions post-discharge. To witness a visible and landslide impact in chronic care management, providers must be looking for a mechanism that can track care management for high-risk patients beyond the 30-day readmission policy.

Less accommodation for comorbidities

Multiple chronic conditions have associated comorbidity that can increase the costs in the long run. Healthcare needs to inch to a robust system that takes into account the needs of comorbid patients. Mckinsey research suggests that 71% of patients with heart failure have hypertension, 37% have diabetes, and 53% have hyperlipidemia. These stats indicate that providers have the opportunity to go upstream and engage with these patients while they have a low-morbidity condition.

Inadequate risk stratification

Risk stratification is majorly centered on the needs of high-risk patients and often negates rising-risk patients. While preventive mechanisms for “high-risk” and “rising-risk” patients require a demarcation, specialty care and telehealth don’t promise a similar ROI for both patient pools. Aside from this, additional factors such as Social Determinants of Health are not an integral part of every risk stratification algorithm that results in skewed chronic care management plans.

Fragmented care delivery

A lack of coordination renders chronic care management ineffective and many a time, patients end up receiving clashing treatments that can lead to increased costs.

Primary care vs. specialty care

Primary care providers often face a hard time figuring out when a patient can be successfully managed in a primary care setting or qualifies to be under specialty care. Taking the right call between the two often becomes the reason for higher costs because of an increase in acute care utilization.

One of the many aspects that insurers focus on to create more value through their health plans is to improve communication with the members. In the era of growing digitization, most payers have started to offer online services. However, many beneficiaries still use traditional channels to interact with insurers.

Does it imply that members are averse to using digital channels for communication?

Absolutely not!

On the contrary, members are, in fact, more inclined to using digital channels than ever before. A survey revealed that 77 percent of consumers would like to pay their health insurance bills through an online portal. If members have the option to use digitized modes and they still continue to use the traditional modes, it clearly indicates there is a problem.

What prevents beneficiaries from using digital channels?

At this point in time, multinational giants such as Amazon and Google have made customers accustomed to unbeatable customized digital content. If members are still using old forms of communication, that is bad news for health plans. The probable reason behind this is unsynchronized information on offline and online channels.

Take an example of a member who has been communicating with their insurer through a call center and wants to shift to online communication. For that, they would have to share all their details on the new channel all over again, despite the fact that their information was already available to the insurer. This may lead to frustration because this interaction is neither convenient nor fast. As a result, they wouldn’t want to switch to a channel that makes the process more cumbersome than before.

The solution? Building omnichannel capabilities

For digital channels of communications to thrive and boost member experience, payers must work on developing omnichannel capabilities. Omnichannel communication can allow members to switch seamlessly between online and offline channels at their own convenience, without any additional steps. Even though most health plans offer digital communication, can only creating omnichannel communication maximize its value?

“Pop health is still a pretty manual process. Having a dedicated solution, let alone a dedicated analytics platform, to address pop health is not as widespread as one might think.” — Brendan FitzGerald, research director, HIMSS Analystics

When I first heard this line, a number of thoughts came rushing into my mind around the different population health management strategies deployed today. In my experience, I’ve noticed a lot of variance in these strategies, and somehow, all of them traced back to data integration.

Some regions focus on leveraging their existing EHRs solutions. Other areas attempt to find the best point solutions and try to integrate them together. Many other organizations are looking for partners to help build and deploy more targeted solutions. Ultimately, these organizations are trying to find the right solution to achieve sustainability in these changing times.

Healthcare data: The problem of plenty and inefficient solutions

One problem that I usually see is that there has been a lot of talk around providing a holistic solution — and the industry isn’t even close. Healthcare organizations have already drained millions of dollars in the hopes of improving outcomes through new technologies, and I think there is a dire need for a change in what we promise to deliver. What organizations need now are infallible strategies that focus on achieving a better outcome.

It is never about just integrating the healthcare data!

There is a buzz in healthcare around aggregating data. However, they are far from making sense of this data.

The question which we should be asking right now is how we can help save money and continue to deliver better care. The easiest way to analyze the progress of organizations is by examining the returns on investment in terms of outcomes and revenue. And this return is only possible if organizations are successful in activating this data to ensure that every member is utilizing it to their fullest potential.

Unless healthcare members have a holistic pool of information regarding every activity in their healthcare network, they cannot ensure that they remain at the top of every process.

Taking long leaps to establish transparency in healthcare

A few months back, a tweet from the CMS Administrator, Seema Verma, took everyone by surprise, and the concept of siloed healthcare took a significant hit. Value-based care is the future, and #WheresThePrice laid the foundation for transparency in terms of cost, expenditure, quality, and data.

It is time we took this concept of transparency to a broader level, moving beyond merely the pricing to ensure the transparency of healthcare data. After all, only the right access to the correct data can result in the right outcomes.

By Abhinav Shashank, CEO,

By Abhinav Shashank, CEO,

Source:

Source: