With hundreds of thousands of clinical trials currently underway worldwide, we are continuously seeing innovation applied to how we treat and cure diseases, but the traditional four-phase method of getting there has not been updated since 1963. What makes this antiquated process for pharmaceutical companies and long wait time for patients in need worth it is the promise of a safe and effective therapy for the vast majority of patients.

This promise, however, is negated before the clinical trial begins when pharmaceutical companies opt to perpetuate the creation of blockbuster treatments for the “average” patient that disregards individual patient disease biology.

The cost of ineffective treatment for both patients and the healthcare industry is high in many ways, and there is a clear need to change the process to bring more effective treatments to market. The current system was developed to provide blanket treatments for a particular disease without considering the disease biology of individuals. Moving forward, pharmaceutical companies first need to study the individual’s disease and then create a personalized treatment for patient subgroups within each therapeutic area.

Precision medicine technology holds the key to meet this need and could change the current clinical trial system that has been in place for years. Companies are working on technology such as this to enable more targeted trials that are smaller, nimbler, equally as effective and safe, and encourage the creation of personalized treatments to finally break the cycle of expensive, ineffective blanket treatments.

Enabling smaller, more effective and affordable trials

For years, patients and doctors have started to become exasperated with this traditional, slow-moving clinical trial model and are searching for a more personalized route as an alternative. Precision medicine offers the unique ability to deeply understand the genetic makeup of patients’ diseases, which in turn would enable the development of better drugs with clinical trials that consist of sample sizes based on genetic disease make-up rather than phenotypic expressions.

Backed by preliminary research into the patients being treated, these smaller and more targeted trials can hypothetically be conducted more rapidly and at lower costs, allowing for breakthrough therapies to come to market faster at potentially more affordable prices.

A key element in achieving end-to-end revenue cycle success in any healthcare operation is proper dedication and maintenance of workflow tools, and those systems that support processes that help organizations meet net revenue expectations.

Workflow optimization and the deployment of tools should be viewed from four perspectives: People, process, technology and metrics/KPIs/reporting.

It is incumbent on healthcare organizations to explore each of these areas related to RCM workflow optimization and consider relevant questions before deploying a fresh approach to workflow processes and automation. First, they must recognize that a balance of concentration of these four components is needed when building operational effectiveness and for the success of workflow strategy, tools and support systems. Furthermore, it is critical for RCM workflows (front, middle and backend) to reflect the uniqueness (location, size, demographics, payer mix, etc.) of the organization.

While there are many benchmarks and strategies in the industry that an organization can follow, adapt to or adopt, the specific characteristics of the organization – whether it’s a rural versus urban facility, the size and makeup of its staff, budgets, effects of recent mergers and acquisitions, and more – must be inputs when building and maintaining effective workflow controls. Principally, dedication to establishing optimization in workflows within revenue cycle operations is a direct result of senior management’s objectives of lowering or maintaining organizational metrics involving departmental and organizational “cost to collect”.

Organizations’ achievement of desired “cost to collect” results comes from their empowerment of senior and middle management and line staff, adoption of sound strategies that are understood and embraced, provision of user-friendly processes and effective deployment of technology – as well as maintenance of technology in a manner that is adaptable and flexible to the user and the organization.

More importantly and in support the first three components, organizations pursuing workflow optimization must have a process in place for measuring and gauging the success of established RCM goals, as well as clear metrics. Metrics are where the rubber meets the road – they’re how organizations know whether the people, process and technology components are functioning efficiently and as intended.

As in any situation where there is a desire to get from one point to another effectively and efficiently, a sound understanding of how metrics support organizational expectations will inform the direction and strategy. It is also important to note that RCM workflow optimization is system agnostic. While each organization has different approaches to workflow support and automation, they need to look at this component relative to the system they have deployed as well as their own uniqueness.

With a dedicated, all-encompassing approach to workflow operations, organizations are better positioned to process patient access, improve eligibility/benefits verification administration processing, improve Point-of-Service (POS) collections, effectively manage claims loads, process appeals in a more timely manner and improve self-pay production and collections. They can also maintain proper coding requirements, improve overall processing, and possibly reduce denials or denial rates, all while improving overall aspects of the revenue cycle continuum to achieve organizational strategic and revenue goals.

While there is no off-the-shelf, cookie-cutter formula to deploy to achieve expected net revenues and RCM optimization, establishing and maintaining benchmarks consistent with the uniqueness of an organization is key to success.

Organizations must address many questions to understand whether workflow operations and technology are hitting the mark. While a holistic approach taking into account people, processes, technology, and metrics is fundamental for true system effectiveness and performance optimization, there are many considerations associated with each of these areas.

People/Resources:

Does your staff have the capacity to perform production requirements needed for organizational success? Additionally, in deploying resources, are team members in the right positions? Are there leaders who can enable others’ success?

Do all RCM staff fully understand their roles relative to the RCM end-to-end continuum? Are staff interchangeable or cross-trained to increase operational understanding or in preparation to fill unexpected gaps?

Does RCM management deploy outsource resources as a stopgap measure?

Are teams looking at “root cause” issues that will affect workflow production goals and objectives?

Processes

In the case of new RCM systems and upgrades to present systems, are workflow processes reviewed or challenged with respect to potential changes in technology?

Are RCM operational workflow processes interchangeable so that any new introducing effects do not create abnormalities, gaps, and workarounds?

Does the organization embrace outsourced help in achieving best practices in workflow processes?

Should the organization consider a central billing office if one does not exist?

While there are more questions organizations ought to consider in reviewing – and correcting – the effectiveness of the RCM continuum, the areas of people and process should guide the use of resources in the most efficient and effective manner. Furthermore, the structure of operations should allow for adaptable departments(s) and an environment that promotes the achievement of organizational goals and the ability to manage expected and unexpected changes.

By Abhinav Shashank, president and co-founder, Innovaccer.

Abhinav Shashank

What makes anyone identify the best health plan for themselves? In today’s world, having health insurance is very important. You might end up paying significantly more for a doctor’s visit if you don’t have insurance than if you had it. You could rack up paying hundreds of dollars for a major injury or if you go for a costly treatment. And in this flock of health insurances, employer-sponsored health plans make up a significant percentage.

How does employer-sponsored health plans fit into the situation?

Employee health and well-being is not just essential, but also foundational to business success. Only a healthy team could deliver profitable outcomes. For this reason, among the list of many, most of employed Americans have their health insurance covered by their employers.

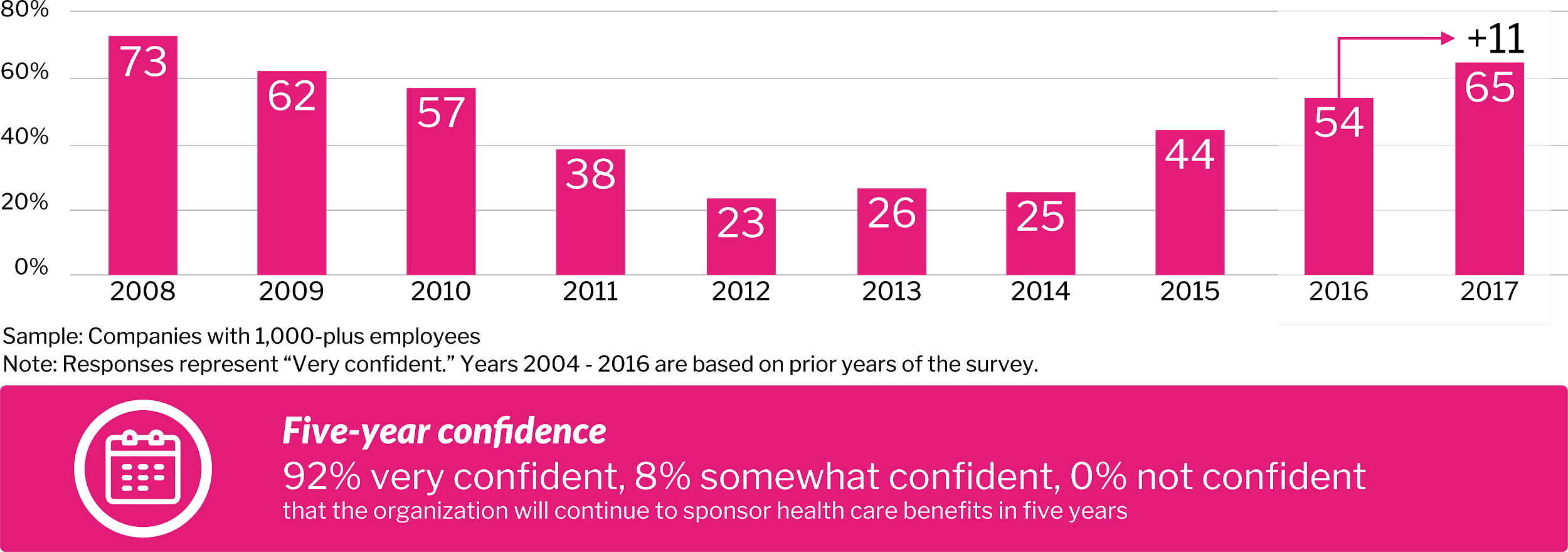

According to a survey, 92 percent of respondents were confident that their organization will continue to sponsor health care benefits for the next five years.

High-performance Insights- Best Practices in Health Care, 2017 22nd Annual Willis Towers Watson Best Practices in Health Care Employer Services

Is employer-sponsored healthcare on the verge of breaking or is it broken already?

Employer-provided healthcare is underleveraged. Currently, employer-sponsored healthcare is facing a lot of complications, including:

New market entrants add more complexity to employer decisions

As financial responsibility for care shifts to employees, an increase in self-rationing may drive poor outcomes

Pharmacy remains an area of unchecked rising cost, especially with regard to high- cost biogenetic (specialty) drugs, among many

What is haunting the large employers and how is the market ripe for innovation?

“Interestingly, 70 percent of employers believe new market entrants from outside the healthcare industry are needed to disrupt health care in a positive way. These disruptors include innovators from Silicon Valley and elsewhere, and employer coalitions,” said Brian Marcotte, president and CEO, National Group on Health.

Fifty-five percent of employers are concerned about prescription opioid abuse and working with partners to implement safe prescribing patterns and alternative therapies. The innovation we need to resolve this issue starts with data. With the launch of CURES 2.0 database, healthcare in the state of California achieved a milestone in curbing the opioid epidemic.

The role of activated data in enhancing the employer-sponsored health plan is that of an initiator to a revolutionary change in the field. Once the organizations have the right data, they can gain crucial insights into their employees and devise better plans to enhance their health and productivity.

In the face of this growing healthcare demand, the supply of medical generalists has been consistently trailing the supply of specialists. By 2030, a study from the Association of American Medical Colleges estimates a shortfall of between 14,800 and 49,300 primary care physicians, as well as a shortage in non-primary care specialties of between 33,800 and 72,700 physicians.

Compacting this issue, the U.S. population is estimated to grow nearly 11 percent by 2030, with those age 65 and older increasing by 50 percent. As physicians begin to retire too, this problem will be exacerbated.

While digital technology has been positively impacting access to healthcare services for quite some time, efficiencies, such as virtual care, need to be implemented widely in order to address the impending physician shortage, and maximize the delivery of quality care.

This implementation will be somewhat natural as patient access and services continue to evolve from live voice interactions to leveraging digital solutions. Several healthcare providers have made this step toward virtual care already, and are showing strong results for patient satisfaction.

A virtual visit pilot program conducted by Brigham and Women’s Hospital found a 97 percent satisfaction rate among patients with access to these new communications and care options, with 74 percent stating “that the interaction actually improved their relationship with their provider.” They also found that 87 percent of patients said they would have needed to come into the office to see a provider face to face if it weren’t for their virtual visit.

Kaiser Permanente Northern California (KPNC) have a similar offering, providing a suite of apps enabling members to exchange secure messages with their clinicians, create appointments, refill prescriptions, and view their lab results and medical records. As a result, the number of virtual visits has tripled to 10.5 million over last six years.

At Valley Health, a tele-ICU has provided a viable solution to reduce mortality rates. During the first year of its implementation, the technology helped save 125 lives, reduce ICU length of stay by 34 percent, and also reduce the sepsis mortality rate.

These examples show how virtual care can aid patients for when they first need help, but the care journey does not stop there. It continues with prescriptions, labs, imaging, and referrals to other care providers. In these instances, virtual care can be used as a follow-up and check-in tool so that patients no longer need to visit their physician in-person, they can quickly interact with them from the comfort of home.

America’s healthcare system is notoriously disjointed, with patchwork information technology and disparate data. The quest for interoperability as an answer – the ability to easily share health records between sites of care – has had varying levels of success. But it’s a solution that is crucial to healthcare’s value-based transformation and can’t be allowed to fail, especially by going too slow to be meaningful.

The challenges associated with interoperability – from fragmented sources of patient information to data being kept in varied formats, to difficulties using an electronic health record (EHR) as a secure central “home” for a patient’s data – were highlighted in a recent American Hospital Association (AHA) report on “The Hospital Agenda for Interoperability.”

The report highlighted challenges for providers and underscored that a collaborative approach is necessary for improving the lives of families and their caregivers for the long-term. The AHA report not only represents frustrations with EHR and Health Information Exchange (HIE) but calls for extending efforts at digital transformation that logically layer on top of that.

As the debate and progress inches forward to 2020, it is vital to return to what hospitals are telling us.

Beyond technical challenges

The difficulty in interoperability goes beyond technicalities. For example, while healthcare providers generate clinical data and payers create claims data, their current structures are not conducive for synchronization and insight generation. Payers and providers have different objectives (whether it’s clinical notetaking, billing, clinical decision support, etc.) so there’s more to the underlying friction than just a variety of data formats.

The AHA calls out additional reasons for issues with interoperability and the high costs that result. That includes expensive workarounds, overcomplicated user interface design, lack of documentation consistency, unrealistic expectations for technical solutions, issues with regulatory compliance for data security, privacy and use, and pricing models that “toll” information sharing. It’s also clear that business and technical challenges with interoperability should not be conflated – each technology Band-Aid further burdens healthcare organizations with ad hoc, un-intuitive technology that will cost more over time and fail to solve interoperability challenges.

In the quest to use technology to save money, improving interoperability between healthcare systems and using powerful data analytics to extract insights from systems working in concert appears to be an expensive and elusive goal. But the cost of not committing to a more universal approach is far greater, because it prevents clear and effective insights on where improvements are needed. Insights are only ever as good as the data that feeds them, and if there isn’t a clearly defined data analytics and data governance strategy aligned with industry best practices, the results will be half-baked.

The need for leadership

Leaders who may have not been exposed to technology outside of healthcare may not be aware of open source, cloud-based tools to rapidly and more cost effectively meet interoperability needs. As they implement piecemeal or outdated, point-to-point solutions, technology costs rise significantly, while perception of technology’s efficacy goes out the window. Worse, paying to ship data to third-party vendors instead of focusing on an internal and overarching connectivity strategies involving every vertical means opportunities to maximize their data’s potential will be lost.

In other words, healthcare organizations might find that they are ironically spending immense amounts of money on technology intended to reduce costs under a value-based payment system. But they might not be spending it wisely. And as other industries steam ahead with movements akin to interoperability on a national scale, leaders in healthcare need to stay focused on the larger task of consistency as not to fall even further behind. Unlike industries like retail, the quality of lives for patients and their caregivers are at stake.

Technology – and business – challenge

As the AHA report emphasizes, the challenges involved go beyond technology and land firmly in the realm of business. Healthcare organizations need to be open to making health data available, whether it’s a secure transfer to another provider, or to the patients. CMS recently renamed “meaningful use” to “promoting interoperability” in efforts to provide a model and further incentives for “advancing care information.”

In the United States, there are approximately 40 million patients with kidney disease; 450, 000 of these patients are on dialysis. However, dialysis treatments can be lengthy, expensive, and not fully covered by insurance – leading to many complications for kidney patients. In addition, dialysis is not a good long-term solution for kidney disease, leading to the development of several other diseases and conditions. Why do kidney failure patients need dialysis, and how can we prevent the prevalence of kidney complications in the United States?

What is dialysis?

Our kidneys are an organ that our body uses to filter waste from foods, medications, and toxic substances that may enter our system. They make urine to remove wastes from our blood and extra water from our body to help us stay healthy. Kidneys are also important in maintaining your overall fluid balance and regulating the minerals that circulate throughout your body. They also produce helpful hormones that control red blood cells, bone health and blood pressure regulation.

When your kidneys shut down due to kidney complications, you cannot maintain these key bodily functions. More than 8 million Americans suffer from chronic kidney disease, according to the nonprofit Wait List Zero. Of these patients, approximately 450,000 are undergoing dialysis, the only treatment that can keep them alive. Dialysis is a treatment that replaces some kidney functions by:

Regulating blood pressure

Removing waste, salt, and excess water to prevent buildup in your body

Regulating levels of certain chemicals in your blood, such as bicarbonate, potassium, and sodium

The current cost of dialysis

Dialysis is a lengthy and intensive procedure, with many patients attending three sessions a week at four hours each. It only performs about 10 percent of a kidney’s function, making it a short-term life-saving solution that is not suitable for long-term treatment. Only 33 percent of dialysis patients live past five years. One in four patients passes away within 12 months.

We live in a world where medical errors are the third leading cause of death behind cancer and cardiac disease, leading to more than 200,000 preventable deaths every year. We have an aging population growing at an unprecedented rate: 8.5 percent of people worldwide (617 million) are aged 65 and over, and this percentage is projected to jump to nearly 17 percent (1.6 billion) by 2050, leading to an anticipated physician shortage of more than 50,000 by 2025.

On top of all of this, healthcare costs are projected to increase to over 25 percent of GDP in the United States by 2025. The convergence of these events is pushing the entire industry to begin leveraging technology more than it has in the past.

Many of these challenges can be remedied by leveraging industrial IoT (IIoT) technology that’s been proven to solve similar challenges in other industries. Could an interoperable, connected healthcare platform that applies the principles of an IIoT connectivity architecture to share data throughout the healthcare system be the cure for our ailing healthcare system?

West Health, now the Center for Medical Interoperability, seems to think so. In 2013 they published a report showing how an interoperable, connected healthcare system could provide nearly $30 billion in industry savings while improving patient outcomes in the process. These connected healthcare platforms provide the foundation for innovation that is needed to make a meaningful data-driven change in healthcare. It’s these platforms that open the door to application developers everywhere to create modality-specific applications using artificial intelligence and machine learning.

So what exactly is a connected health platform and how does it provide a foundation for transformational change in healthcare? First, a connected health platform consists of hardware (gateways and servers) and embedded software components that are designed to take all of the data from any medical device (clinical or remote) and convert the data in a single usable format that gives providers access to a complete data set.

This connected platform will provide a variety of user interfaces, analytics and clinical applications to help users throughout the healthcare ecosystem distill value from this newly-gathered data. The applications range from the early detection of sepsis, to predicting cardiac arrest, to providing business analytics like bed and device utilization.

The connected health platform will become the center of an ecosystem for further application development, similar to that of an online app store — but with built-in medical-grade safety and security. The connected health platform must ensure data security and patient privacy by aligning to guidance provided by the FDA on cybersecurity, and meeting the standards defined by HIPAA.

However, these connected health platforms are only as effective as the data they capture, which is determined by the connectivity frameworks they are built upon. Many of the currently deployed platforms are not platforms at all, but a collection of disparate systems that provide silos of individual device data. These legacy systems have been built using internally-developed, proprietary, message-based communication technology.

As the first step towards the development of a connected health platform, modern web services-based communication has been deployed on top of the legacy technology to begin integrating all of the disparate data streams via onsite data centers or the cloud. Although this is a step in the right direction, these platforms are far from complete. Because of legacy communications infrastructure they are built upon, they are only able to aggregate a portion of the data making these systems a poor fit for true near-patient, real-time clinical decision support – the key to efficiently providing improved patient outcomes.

The EMEA market for electronic health record (EHR) IT is estimated to have been worth $3.7B in 2018 (both acute and ambulatory applications) according to Signify Research’s 2019 global EMR market report. However, only one vendor, Cerner, is estimated to have had a double-digit revenue share in 2018. In terms of suppliers the EMEA market is highly fragmented with a mixture of local and international vendors addressing individual countries with few vendors having a truly region-wide footprint.

The table below shows estimated revenue shares in 2018 for the acute & health system EHR market in EMEA (excluding revenues for ambulatory only solutions), alongside the countries/sub-regions where each vendor had a significant share of its EMEA business.

Acute/Network EHR Estimate Revenue Share – EMEA – 2018

2018 Rank

Company

2018 Revenue Share

Key Countries/Sub-Regions

1

Cerner

16%

DACH, UK/Eire, Middle East

2

Agfa Health

8%

DACH, France

3

Asseco

5%

Eastern Europe

4

CompuGroup Medical

5%

DACH, Nordics, Eastern Europe

5

InterSystems

4%

UK/Eire, Middle East, Spain/Portugal

6

Chipsoft

4%

Benelux

7

DXC Technology

3%

Benelux, UK/Eire, Spain/Portugal

8

Tieto

3%

Nordics

9

Dedalus

3%

Italy, France, Spain/Portugal

10

Nexus

3%

DACH, Benelux

11

Engineering Ingegneria

3%

Italy

12

Systematic

2%

Nordics

13

Epic

2%

Benelux, Nordics, UK/Eire, Middle East

14

Telekom Health

2%

DACH

15

Maincare Solutions

2%

France

Others

39%

Source: Signify Research

Note: Does not include ambulatory only revenue/vendors

In the United States, there are approximately 40 million patients with kidney disease; 450, 000 of these patients are on dialysis. However, dialysis treatments can be lengthy, expensive, and not fully covered by insurance – leading to many complications for kidney patients. In addition, dialysis is not a good long-term solution for kidney disease, leading to the development of several other diseases and conditions. Why do kidney failure patients need dialysis, and how can we prevent the prevalence of kidney complications in the United States?

In the United States, there are approximately 40 million patients with kidney disease; 450, 000 of these patients are on dialysis. However, dialysis treatments can be lengthy, expensive, and not fully covered by insurance – leading to many complications for kidney patients. In addition, dialysis is not a good long-term solution for kidney disease, leading to the development of several other diseases and conditions. Why do kidney failure patients need dialysis, and how can we prevent the prevalence of kidney complications in the United States? We live in a world where medical errors are the third leading cause of death behind cancer and cardiac disease, leading to more than

We live in a world where medical errors are the third leading cause of death behind cancer and cardiac disease, leading to more than